Calculate Compound Interest in Excel

Making excel spreadsheet

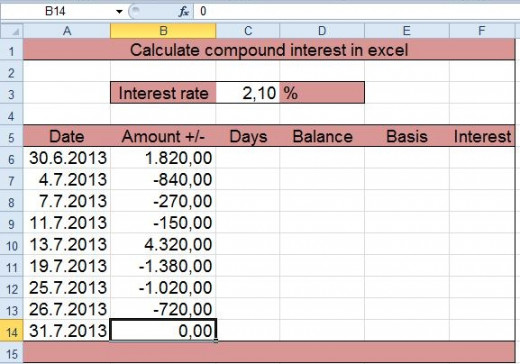

Please consider of line and columns, that you will be being able to copy formulae.

Enter the interest rate, as well as all the dates and amounts. The beginning of period represents first date; amount of balance is put on this next to him. Enter dates, when you had the inflow or outflow. Last date is the date on which the period ends for which you counting interest. The amount of the last data is zero; it does not affect the calculation of interest.

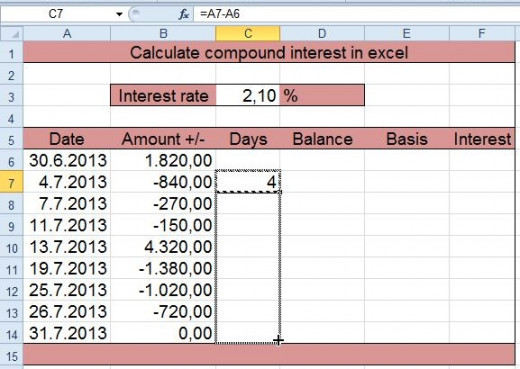

Calculate number of days

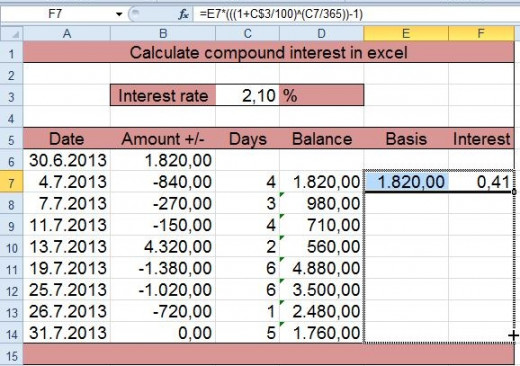

Calculate the number of days when the balance is not changed, from the current date minus the previous. In cell C7 copy the formula = A7-A6. Then copy the contents of the cell in all below it.

In the calculation we take into account the rule that takes into account the first day and the last is not. If you count interest from yesterday to today, it would count for one day, and that interest should be accounted for on the balance, which was yesterday.

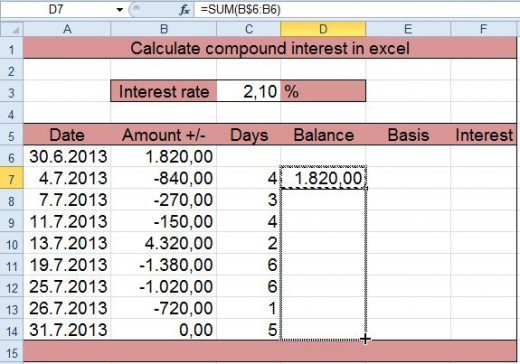

Calculate balance

Balance is the sum of the initial state and all changes. The formula =SUM (B$6: B6) copied into cell D7. $ on the first cell, so that the row when copying will not be updated (it will always B6). Cell is copied in all below it. The balance does not take account of interest from the previous period.

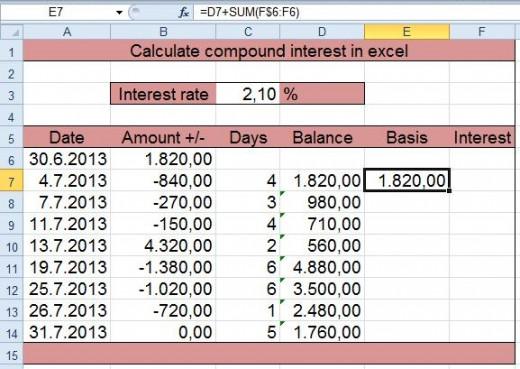

Calculate basis

Specialty method of calculating compound interest is the fact that the basis for calculating interest is added to the interest calculated in the previous period. Thus, they form the basis for calculating the base from the previous period, the change in the current day and the interest from the previous period.

The basis for the calculation of interest shall be calculated by dividing the balance of all interest in the previous period. In cell E7 copy the formula =D7 + SUM (F$6:F6).

You calculate

Calculate compound interest

Copy the formula =E7*(((1+C$3/100)^(C7/365))-1). Then highlight both cells (E7 and F7) and copy them to all of the following.

We must pay attention, that at leap year instead of 365 use 366. If period stretches after more years, we distribute it at the end of year.

Which loan are more expensive if the accounts several times a year?

Calculate total interest

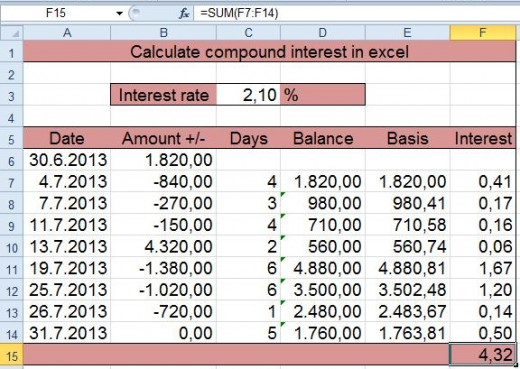

All interest must add. This is done with the function =SUM(E7:E14). You need to adjust the formula according to how many periods it was in your case.

Mortgage Calculator with Extra Payments

- Mortgage Calculator with Extra Payments - Mortgage Calculator

Try different options and combinations of regular or non-regular extra payments and find out how and when you can pay off your mortgage.

The answer to the question of research

Which loan is more expensive if the accounts several times a year?

The more expensive is the loan with a simple method of calculating the interest. This is illustrated by the following table.

Wording

The impact of intensifying relies on upon the recurrence with which hobby is aggravated and the occasional interest rate which is connected. Along these lines, to precisely characterize the add up to be paid under a legitimate contract with hobby, the recurrence of exacerbating (yearly, half-yearly, quarterly, month to month, day by day, and so forth.) and the interest rate must be indicated. Distinctive traditions may be utilized from nation to nation, however in money and financial aspects the accompanying uses are basic:

The intermittent rate is the measure of interest that is charged (and along these lines intensified) for every period isolated by the measure of the key. The intermittent rate is utilized essentially for figuring’s and is once in a while utilized for correlation.

The ostensible yearly rate or ostensible interest rate is characterized as the intermittent rate increased by the quantity of aggravating periods every year. For instance, a month to month rate of 1% is identical to a yearly ostensible interest rate of 12%.

The successful yearly rate is the aggregate amassed interest that would be payable up to the end of one year separated by the foremost.

Financial analysts by and large want to utilize successful yearly rates to improve correlations, however in fund and trade the ostensible yearly rate may be cited. At the point when cited together with the aggravating recurrence, an advance with a given ostensible yearly rate is completely indicated (the measure of enthusiasm for a given advance situation can be definitely decided), yet the ostensible rate can't be straightforwardly contrasted and that of credits that have an alternate intensifying recurrence.

Credits and financing may have charges other than hobby, and the terms above don't endeavor to catch these distinctions. Different terms, for example, yearly rate and yearly rate yield may have particular lawful definitions and could conceivably be equivalent, contingent upon the ward.

The utilization of the terms above (and other comparative terms) may be conflicting and change as indicated by neighborhood custom or promoting requests, for straightforwardness or for different reasons.

The difference between compound and simple method

Interest rate

| 10

| amount

| 10000

|

Days

| compound interest

| simple interest

| difference

|

30

| 78.64

| 82.19

| 3.55

|

60

| 157.91

| 164.38

| 6.48

|

90

| 237.79

| 246.58

| 8.78

|

120

| 318.31

| 328.77

| 10.46

|

150

| 399.46

| 410.96

| 11.50

|

180

| 481.24

| 493.15

| 11.91

|

210

| 563.67

| 575.34

| 11.67

|

240

| 646.75

| 657.53

| 10.78

|

270

| 730.48

| 739.73

| 9.24

|

300

| 814.87

| 821.92

| 7.05

|

330

| 899.93

| 904.11

| 4.18

|

360

| 985.65

| 986.30

| 0.65

|